Key ‘26 Tax Changes and What They Mean for You

If you would like to consider building a personalized Prosperity Financial Plan, don’t hesitate to reach out. Schedule a Meeting

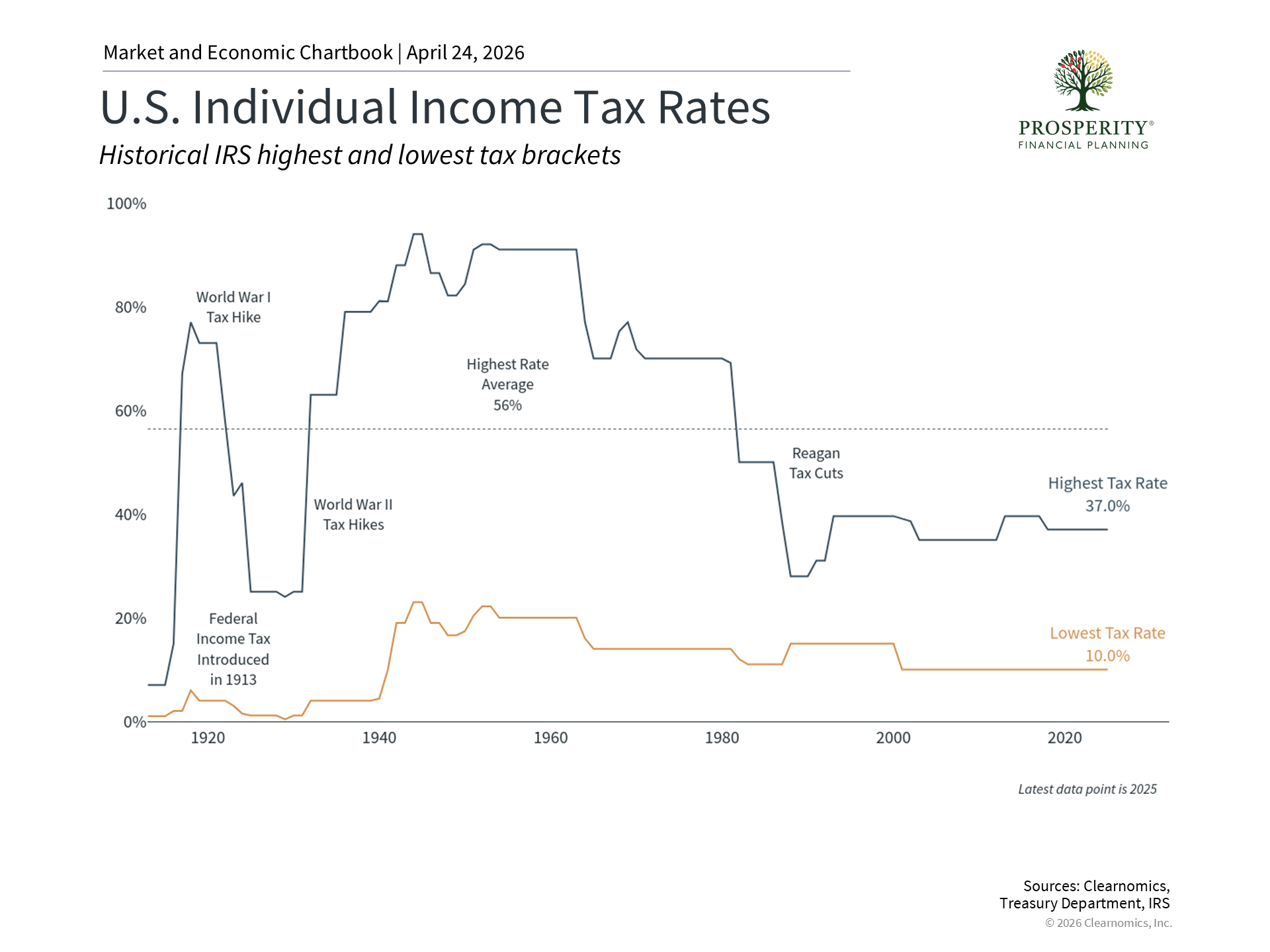

Phew! You’ve recently finished up your 1040 and noted how much you paid to the I.R.S. While the U.S. remains at relatively low individual income tax rates, you may be wondering if now’s the time to do some Roth conversions or other ways to minimize your future tax bite. 2026 brings meaningful changes to U.S. tax policy that open up new planning opportunities. From updated retirement savings rules to higher deduction limits, being aware of these shifts can help you make smarter financial decisions.

While the 2026 tax policy changes may not universally apply to everyone, it's worth reviewing which may be relevant to you, your family, or others in your community. Please don’t hesitate to reach out if I can help.Catch-up contributions now have new Roth requirements

If you are 50 or older, you are allowed to save extra money in your retirement account beyond the normal yearly limit — these are called "catch-up contributions." Starting in 2026, if you earn $150,000 or more per year, these extra contributions must be made as Roth contributions. That means you pay taxes on the money now, but it grows tax-free and can be withdrawn tax-free in retirement. The standard catch-up limit has increased by $500 to $8,000 for those aged 50 and older, while the "super catch-up" for ages 60–63 stays at $11,250.For high earners who previously used pre-tax catch-up contributions to reduce their current tax bill, this change means a higher tax bill upon withdrawal. It’s worth reviewing how this fits into your overall financial plan.The SALT deduction cap has increased significantly

The state and local tax (SALT) deduction — which lets you deduct certain taxes you pay to state and local governments — has been raised from $10,000 to $40,400 for 2026, and will increase by 1% each year through 2029. This is especially helpful for people living in high-tax states. The standard deduction (a flat amount anyone can claim without listing individual deductions) is $16,100 for single filers and $32,200 for married couples filing jointly in 2026.Since the cap was set at $10,000 back in 2017, far fewer people found it worthwhile to itemize their deductions — meaning listing out individual deductible expenses rather than taking the standard deduction. The share of taxpayers who itemized dropped from about 30% before 2017 to just 10% in 2022. With the higher cap, many more households may now save money by itemizing. Keep in mind that this higher cap is temporary and is scheduled to revert to $10,000 in 2030.How these changes connect to retirement planning

Tax changes rarely work in isolation — they can affect other parts of your finances too. For example, if the new Roth catch-up rules raise your taxable income (the amount of income subject to tax), more of your Social Security benefits could become taxable as well.There is also a new "senior bonus" deduction of $6,000 for single filers or $12,000 for married couples aged 65 and older, available for tax years 2025–2028. However, this benefit phases out at higher income levels, so decisions that increase your taxable income could reduce or eliminate this deduction.The expanded SALT deduction also creates planning opportunities. If you are close to the point where itemizing makes sense, strategies like grouping charitable donations into one year or prepaying property taxes (where permitted) could help you benefit further.As always, I’m here to discuss how these changes may apply to your specific situation. Please don’t hesitate to reach out with any questions.The bottom line? The 2026 tax changes introduce both new rules and new opportunities worth reviewing. Understanding how these shifts affect your overall financial picture can help you make better-informed decisions and strengthen your long-term plan.

Important Disclosure Information: This blog is published by Prosperity Financial Planning LLC, a registered investment adviser with the state of Florida and the commonwealth of Pennsylvania. Registration does not imply a certain level of skill or training.

General Information Only: The content provided is for general informational and educational purposes only and should not be considered personalized investment advice. Nothing contained in this blog constitutes a solicitation, recommendation, or offer to buy or sell any securities or other financial instruments.

No Investment Advice: This content does not constitute investment advice and should not be relied upon as such. Any investment decisions should be made only after consulting with qualified financial professionals. Past performance does not guarantee future results.

No Warranties: While we strive to provide accurate information, we make no representations regarding the accuracy, completeness, or timeliness of the content. We do not endorse third-party information and are not responsible for external websites or resources.

Risks and Relationships: All investments involve risk of loss. Reading this blog does not create an advisory relationship with Prosperity Financial Planning. Advisory relationships are established only through execution of a formal investment advisory agreement.

For more information about our services and important disclosures, please refer to our Form ADV Part 2A, available upon request, through the link below in the footer, or at www.adviserinfo.sec.gov.

Contact Information Prosperity Financial Planning LLC, Celebration, Florida. elizabeth@prosperityfinancialplanning.com